Creating a Cashflow Forecast in Calxa

A good portion of your Cashflow and Balance Sheet Forecast is calculated for you in Calxa by using your Profit & Loss budget and the account and timing selections you make in Cashflow Settings for taxes like GST/VAT, PAYG and employee liabilities.

Calxa takes the hard work out of predicting the timing of payments and receipts by analysing your current average Creditor Days and Debtor Days. You can then just add any other Balance Sheet budgets required (i.e. asset purchases/loans) and your 3-Way Forecast will be ready to go.

This help note will will walk you through 5 easy steps to deliver a 3-Way Forecast containing a Profit & Loss, Balance Sheet and Cashflow Forecast.

TABLE OF CONTENTS

Step 1: Profit & Loss Budget

The budget is the single most important aspect of preparing a cashflow forecast. To create an accurate cashflow you require an accurate budget. The minimum requirement is to enter a Profit & Loss (P&L) budget.

The intention of your P&L budget should be to create a reasonable estimate of what will happen in your business. When calculating your Cashflow Forecast, Calxa will use your Cashflow Settings to project the cash and Balance Sheet movements of your budgeted P&L. Since GST Collected and Paid movement is calculated for you, all budget values should be entered exclusive of GST.

Create a budget for the current financial year and next year.

Review your business plan(whether it's a document or something that’s in your head) and adjust the budget accordingly:

Will your income increase or decrease next year? Is this because of something you are planning or external factors?

If your income changes what effect will that have on Cost of Goods Sold, Wages and other expenses?

Think about other changes that might affect your budget.

For help with creating budgets please see the following help notes:

Edit Budgets - to create a new budget or edit an existing one.

Budget Factory - when you don't have a budget yet, you can use the Budget Factory to get started; it's also useful for creating a reforecast containing YTD Actuals plus budget for the forecast months.

Import your budget from a spreadsheet - use this when you already have budgets created in Excel, have a large number of business units, or have complex formulas best modelled in Excel.

Sync the budget from your accounting system - this can be done for both the business unit and organisation level with MYOB AccountRight and QuickBooks Online, and for the Overall Budget only with Xero. See step 5 of each linked article for more details.

Refer also to the Organisation Budget (Consolidation Setting) and Manage Budget Versions help notes.

Step 2: Cashflow Settings (Timing)

Timing is what differentiates a budget from a cashflow forecast. A budget looks at when accounting transactions will take place, but the timing of the associated payments and receipts is often different from the budget.

Much of your Cashflow and Balance Sheet Forecast is calculated for you in Calxa by using your Profit & Loss budget and the account and timing selections you make in the Cashflow Forecast Settings screens.

Navigate to Budgets & Cashflow -> Cashflow Settings.

Review and edit the Cashflow Settings listed below:

Cashflow Settings Summary

For some users, entering a P&L budget and reviewing Cashflow Settings may be all that's required to create a reasonable Cashflow Forecast. However, if you plan to purchase or dispose of assets or acquire and make payments on loans please review Step 3 - Balance Sheet Budget. Otherwise, you can skip to Step 4 - Presentation.

To learn more about how the Cashflow Settings adjust the timing of your budget, continue on to read the section below on Receipts and Payments & Expenses. This section also describes how to handle Grants Received in Advance and Income Received in Advance, as well as Prepaid and Accrued Expenses.

Receipts

The default setting for most Income accounts is Debtor Days. This uses your current average days outstanding debtors to create a profile of receipts, estimating what proportion will be received each month.

Note: This is likely to give the best result for most organisations.

Users can override the Debtor Days count to something other than the average - see point 5. in Cashflow (Basic Settings) for instructions to do this. Alternatively, users could choose to update the setting to Profile via the Cashflow Settings -> Cashflow (Advanced Settings) screen and enter their own timing estimates by month, if preferred.

Not-for-Profits receiving Grants in Advance, or any business with Income in Advance should review this help note for the correct setup for cashflow.

Payments & Expenses

The default setting for most Cost of Sales and Expense accounts is Creditor Days. This uses your current average days outstanding creditors to create a profile of payments, estimating what proportion will be paid each month.

Note: This is likely to give the best result for most organisations.

Users can override the Creditor Days count to something other than the average - see point 5. in Cashflow (Basic Settings) for instructions to do this. Alternatively, users could choose to update the setting to Profile via the Cashflow Settings -> Cashflow (Advanced Settings) screen and enter their own timing estimates by month, if preferred.

Wages and Salary accounts have a cashflow type of Wages tax, which can be set in either the Cashflow Settings -> Wages & PAYG screen or in the Cashflow screen. Wages tax is used to split the budgeted wages between the net wages that are paid out each month and the tax that is withheld and paid to the tax office at a later date.

Taxes such as GST/VAT and Company Tax, and other liabilities such as Superannuation or Pension Plan payments are managed with Schedules that determine the frequency of payments. Users can create customised schedules if the defaults are not suitable.

Prepaid Expenses can be handled similarly to Grants in Advance, where the Prepaid Expense asset account remains set with a cashflow type of Profile (100% Current), and the Prepaid Expense Allocated and related Expense accounts are set to a cashflow type of None.

A simpler option for Prepaid Expense cashflow settings is to ensure both the Prepaid Expense asset account and the related Expense accounts are set to the same cashflow type, whether that be Profile (100% Current) or Creditor Days.

With this option, the monthly amortisation to expense will appear in the cashflow forecast report, however the inflow and outflow will offset each other for zero net cashflow effect (Dr. Expense, Cr. Prepaid Expense Allocated). An impact to cashflow only occurs when the actual payment for an expense is made up front.

Accrued Expenses that are paid on a regular timing can be handled as a scheduled payment. In this case the Expense account has a Cashflow type of None, and the liability account will be set as a Schedule. In this situation you need to budget equal amounts on both accounts to keep your budget in balance (see Balanced Budget below).

Depreciation and Amortisation expenses do not affect your bank, and as a result these accounts have a cashflow type of None. You can set this up using the Depreciation settings screen, where Calxa will create a balancing accumulated depreciation or amortisation budget for you.

Anyone wanting to understand more about how Debtor and Creditor Days are calculated in Calxa can refer to the Creditor and Debtor Calculations help note.

Step 3: Balance Sheet Budget

There are many transactions in the Balance Sheet that will affect your cashflow forecast. Some of them, such as your Trade Debtors, Trade Creditors, tax accounts and employee liabilities are calculated by Calxa. For others transactions you will need to enter some budgets, such as in the case of purchase or disposal of assets, or loan acquisition and payments.

For instructions on Balance Sheet budgeting see this video.

Select your Bank Accounts, Trade Debtors, Trade Creditors and earnings accounts via the Cashflow Settings -> Bank & Equity screen.

Calxa is unable to determine which bank accounts will be used for which transaction, therefore for cashflow purposes multiple accounts will be treated as a combined virtual bank account.

If you have a Cash Management or similar account enter a positive budget amount when you transfer money into it, a negative amount when you transfer money out.

When you enter Balance Sheet budgets for accounts, it is important to understand that the budget values reflect movement in a period. A value in a specific period does not reflect the balance in that period.

A positive budget means that the balance of an account is expected to increase by the budgeted dollar amount in that period. A negative budget means that the balance of an account is expected to decrease.

Add positive budgets for the purchase of new assets and negative amounts for their disposal. Add a positive budget in a loan liability account for acquisition of a loan, and negative amounts for principal repayments.

Since the default cashflow setting for an Asset or Liability is Profile (100% Current), the effect of budgeting on the Balance Sheet is generally a direct relationship with the bank balance. In other words, whatever you budget in a month will be reflected in the cashflow in the same month. If this is not your intention for a particular Balance Sheet budget line, ensure the appropriate Cashflow setting is applied.

Balanced Budget

Accounting rules dictate that debits must equal credits, and the same can be said for your budget. Calxa will keep your debits and credits balanced for you in most cases, however there will be certain circumstances when this is not possible. Namely when budgeting on accounts with a cashflow type of None or Schedule (excluding nominated Cashflow Setting accounts).

For example, to handle Accrued Expenses you might have an Expense account with a Cashflow Type of None and a Liability set to be paid on a Schedule. In this example, Calxa will exclude the budgeted Expense from your cashflow forecast, however Calxa doesn't know where the balancing side of this budget belongs.

With other cashflow types like Creditor Days, the balancing side is a combination of your nominated Trade Creditors and Bank accounts and Calxa handles this for you. In this Accrued Expenses example, we know the balancing budget needs to be on our Accrued Expense Liability account, but there is no setting to tell Calxa which account this is. Instead you must enter the balancing budget manually. Setting the Liability budget the same as the Expense will balance the budget by increasing the Liability with the Expense. The Schedule cashflow type will handle the payment based on the budgeted Liability closing balance.

The most important thing to note is this: If you budget on accounts with a cashflow type of None or Schedule, then you must ensure the budget is balanced. The Budget Discrepancy Analysis By Debits/Credits report will check the balance of your budget. This report will isolate the accounts of interest and their associated budgets to help resolve any balancing discrepancies. For more information on this report refer to the help article – Balancing your Budget with the Budget Discrepancy Analysis Report.

For assistance to understand any unexpected values in your cashflow forecast or Balance Sheet, please refer to the Understanding and Troubleshooting Cashflow help note.

Step 4: Presentation

Cashflow Forecast

Always consider your audience when deciding how best to present your cashflow forecast. Charts are often best for board reports and senior management. They are visual and easy to interpret at a glance.

Search for the Cashflow Forecast Chart in the Report Builder to display this chart.

For those who need reports, consider the level of detail that is required. An accountant may be interested in a Level 4 report with all the detail, but other users may be satisfied with Level 2 or 3 (this will depend on the headings in your Chart of Accounts). If these headings aren’t the most useful, consider using Account Trees to reorder the accounts into something more meaningful for your readers.

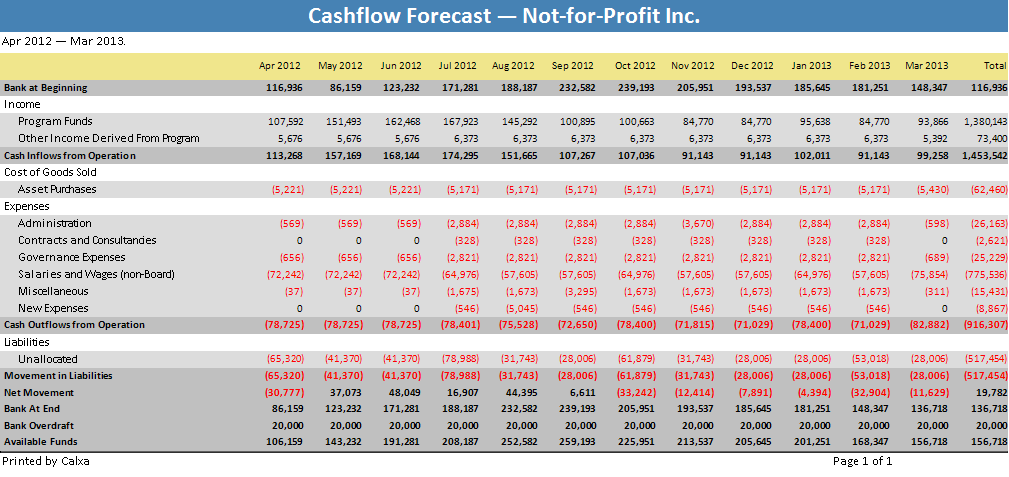

Search for the Cashflow Forecast (Multi Period) in the Report Builder to display this report.

Bank Movement Report

Note the Cashflow Forecast report can be run on forecast periods only, it cannot be run on actuals periods. If you want a report that includes actuals, consider using the Bank Movement (12 Months) report instead. A sample version of this report is attached in the 3-Way Forecast bundle at the bottom of this help note.

This report has a similar layout to the Cashflow Forecast but displays your P&L accounts at the budgeted accrual amounts, it does not adjust for timing differences or gross figures up for GST/VAT. The timing differences and GST/VAT are reflected in the Balance Sheet section of the report in Trade Debtors, Trade Creditors, and GST Paid/Collected. The other main difference between this report and the Cashflow Forecast report is that this report will include non-cash items such as depreciation.

Complete your 3-Way Forecast Reports

You can complete your 3-Way Forecast reports by adding the pre-set Bundle:

See this help note for an overview of the 3-Way Forecast process.

Step 5: Review, Revise, Improve

Expertise in cashflow forecasting comes with time and practice. The more often you forecast, the better you will become. The more familiar you are with the projections for your organisation, the more likely you will be to recognise anything odd and unusual.

Review

Use the Budget Discrepancy Analysis report with the By Debits/Credits template variant to check that your budget balances.

Test your cashflow forecast for reasonableness. Does it meet your expectations? If it doesn't, consider whether you need to revise your budget or adjust the Cashflow Settings.

To understand any unexpected values in your cashflow forecast or Balance Sheet, please refer to the Understanding and Troubleshooting Cashflow help note.

Revise

Using Budget Versions, you can modify your budget as the year goes on and the world around you changes. You can model different scenarios and examine their cashflow effect before committing to major new decisions.

Compare two cashflow scenarios using the Cashflow Scenarios Line Chart template. A sample version of this chart is attached at the bottom of this help note.

Improve

After you have reviewed and revised as noted above, display your 3-Way Forecast reports again to finalise.

You may choose to customise your reports by adding a logo to improve the presentation.